Home Loan Eligibility Criteria: Influencing Factors & Tips to Improve Eligibility

Owning a home is a significant milestone of financial stability in India. However, the process of applying for a home loan can be intricate, especially when you need to understand and check home loan eligibility criteria and whether you fulfill them.

The housing loan eligibility calculator shows what you can afford and where you stand in the eyes of lending institutions. By comprehending the eligibility criteria for home loan, you can set realistic expectations, plan the budget for your dream home aptly, and position yourself favorably to negotiate better loan terms. Moreover, it reduces the chances of loan rejection, which can negatively impact your credit score.

Home Loan Eligibility Calculator

Eligibility Results

Also Read: The Complete Guide to Buy a House

It's crucial to differentiate between 'eligibility' and 'actual loan amount'.

-

Your home loan eligibility is the maximum loan amount a bank or lending institution ascertains that you're capable of borrowing based on factors like net income, age, credit score, etc.

-

The actual loan amount is determined based on the property's value, your down payment capability, loan repayment ability, and other such factors.

In essence, while you might be eligible for a certain amount, the actual loan sanctioned can be less than your home loan amount eligibility.

In this guide, we will unpack the various factors that determine home loan eligibility criteria in detail, for a salaried person as well as a self-employed individual. making sure you are well-equipped to make informed decisions on your journey to homeownership in India.

Table of Contents

- Factors Affecting Home Loan Eligibility

- Home Loan Eligibility Criteria for Salaried Individuals

- Home Loan Eligibility Criteria for Self-Employed Individuals

- How to Improve Your Home Loan Eligibility

- Frequently Asked Questions about Home Loan Eligibility

Also Read: Financial Terms Related to Home Loans You Must Know

Factors that Affect Home Loan Eligibility

When you apply for a home loan, lenders assess your eligibility based on a multitude of factors. These factors determine not only whether you qualify for the loan but also the maximum amount you can borrow.

Also Read: Is it Better to Buy or Rent a House?

Home loan eligibility depends on these factors which can help applicants improve their loan eligibility. Here’s a detailed breakdown:

Age

Most banks have a preferred age bracket for lending housing loans, usually between 21 and 65 years. The younger you are, the longer your home loan repayment period can potentially be.

Credit Score

Your credit report is a reflection of your creditworthiness and is based on your history of loan repayments, credit card bills, and other financial behaviors. A higher score of 750 and above is favorable and can get you better loan terms.

Employment Type and Stability

Income and job stability in employment or business continuity is critical for both salaried & self-employed. Most lenders prefer applicants who have been in the same job or business for a long time (at least 2-3 years).

Income Level

Your annual and gross monthly income plays a significant role to calculate home loan eligibility. Higher net monthly income not only increases your loan eligibility but can also fetch you a better and more attractive interest rates.

Existing Debts and Liabilities

Your current financial commitments like existing loans or credit card debts, will directly impact your home loan eligibility. Lenders assess your Debt-to-Income ratio to ensure you can manage an additional home loan EMI.

Property Value and Type

The property's value, location, and builder reputation can influence loan eligibility. Banks often lend a certain percentage of the property's market value (Loan-to-Value ratio). If the LTV is high, loan amounts can be high, but they vary across lenders & property types.

Down Payment

If you make a substantial down payment (at least 15-20% of property value), it can be a positive signal for banks or lenders. A significant down payment reduces the lender's risk and influences the amount of housing loan and terms.

Loan Tenure Preference

Longer repayment tenure might increase home loan eligibility since the EMI gets spread over an extended period. On the contrary, a shorter loan tenure means higher EMIs but quicker repayment and potentially less interest paid overall.

Rate of Interest

The type of interest rate can alter your home loan EMI amounts and housing loan eligibility and will depend on the lender's criteria and current market conditions. Fixed interest rates offer stability with constant EMIs, while floating rates are linked to market dynamics and can vary.

Co-applicant Details

Having a co-applicant, like a spouse with a steady income, can enhance your loan eligibility. Taking a joint home loan with another earning member of the family helps improve home loan eligibility to avail maximum loan amount.

Employer’s Reputation (For Salaried)

Being employed in a well-established company or MNC can be an advantage as banks view this as employment stability.

Nature and Type of Business (For Self-Employed)

Certain businesses are considered riskier by lenders. Hence, the nature of the business can play a role in determining eligibility.

These factors determine home loan eligibility and working towards optimizing them will make sure prospective borrowers can increase their chances of availing a home loan.

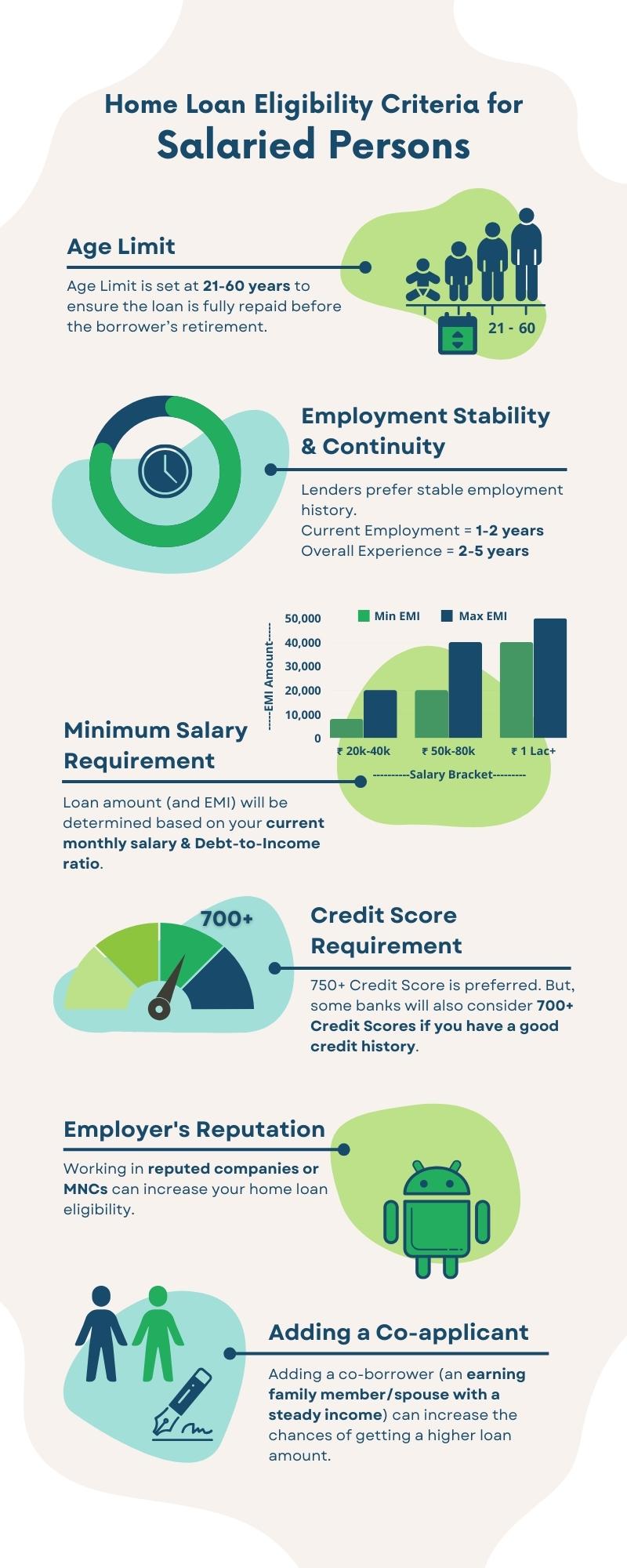

Home Loan Eligibility Criteria for Salaried Persons

For salaried individuals aiming to own their dream home, understanding the specific eligibility criteria for applying for a home loan can be the first step to making that dream a reality. Banks and financial institutions often scrutinize a range of factors when determining a salaried person's home loan eligibility:

-

Age Limit: Typically, the age bracket for eligible salaried individuals is between 21 and 60 years. This is to ensure that the loan is fully repaid at loan maturity before the borrower retires.

-

Employment Stability and Continuity: Lending institutions often prefer applicants who have a stable employment history. Typically, being employed in the current job for a minimum of 1-2 years and having an overall work experience of 2-5 years can be seen as a favorable factor.

-

Minimum Salary Requirement: The monthly salary of a salaried person often dictates the amount of home loan you can avail as it directly affects your repayment capability. These are the loan amounts one can obtain for different salary brackets:

-

Monthly income of 20,000-40,000 INR: For individuals with an in hand salary in this bracket, especially in metro cities, the loan amount might be limited as lenders would ensure that the EMI doesn’t exceed 40-50% of the monthly income. (EMI = 8,000 - 20,000 INR)

-

Monthly income of 50,000-80,000 INR: Individuals in this salary bracket might be able to access high loan amounts. With decent credit reports and minimal other liabilities, securing a substantial loan becomes more feasible. (EMI = 20,000 - 40,000 INR)

-

Monthly income of 1,00,000+ INR: Individuals in this range can often negotiate for better loan terms, including lower interest rates and higher loan amounts, given the financial stability associated with an in hand salary of this income level. (EMI = 40,000 - 50,000 INR)

-

-

Credit Score Requirement: A good credit history can be the golden ticket for salaried individuals. Scores of 750 and above are generally preferred, although some banks might also consider applications with credit scores from 700 onwards.

-

Employer's Reputation: Often overlooked, but the reputation of your employer can influence housing loan eligibility. Individuals working in reputed companies or MNCs are generally in a better position to negotiate favorable loan terms, as employment in such firms is seen as stable.

-

Co-applicant Details: Having a co-borrower, like a spouse with a steady net monthly income, can bolster your home loan eligibility. This can increase the combined income, which can translate to higher loan amounts, as well as share the loan's responsibility.

It's essential to remember that these are general guidelines. Every financial institution may have some differences in their criteria. To increase the chances of loan approval, potential borrowers should aim to align their profiles with these point of reference and always consult directly with lenders to have their home loan eligibility calculated correctly.

Also Read: Why Should You Invest in Real Estate?

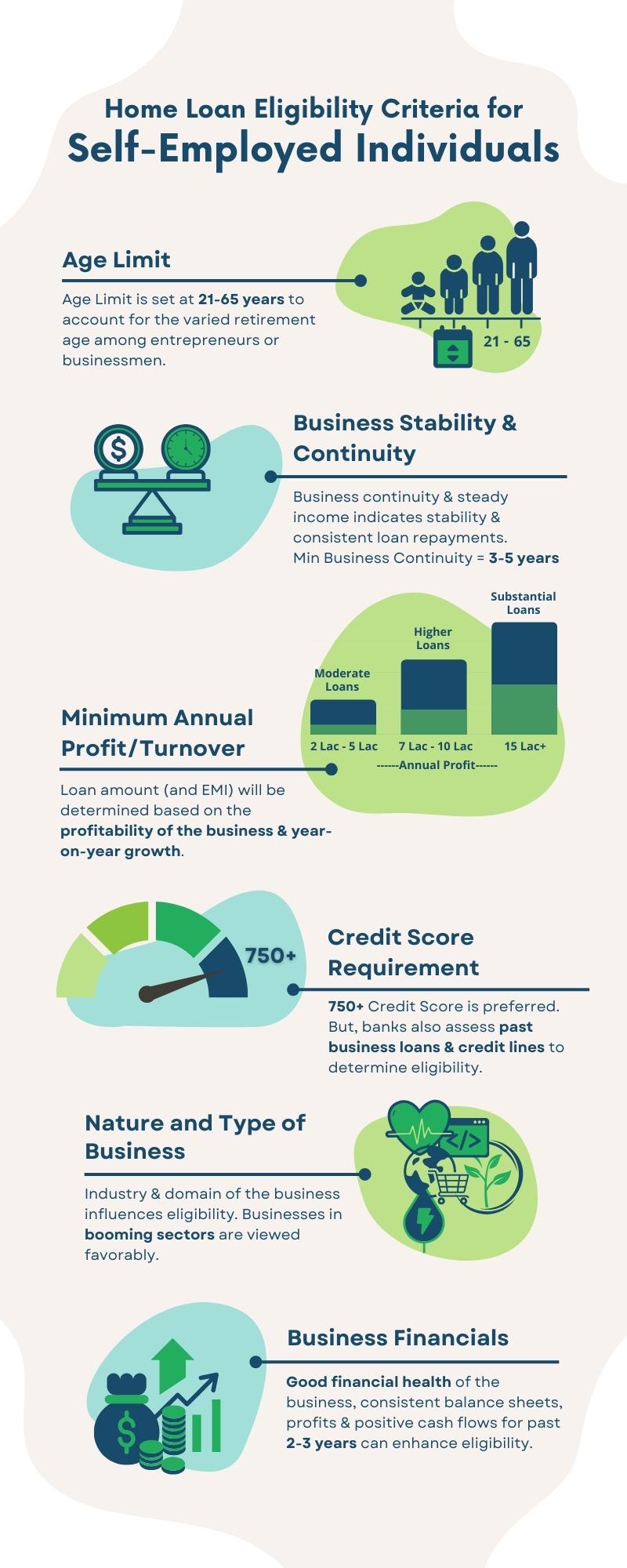

Housing Loan Eligibility Criteria for Self-Employed Individuals

Self-employed individuals, be it business owners, freelancers, or professionals, often have a distinct financial profile. When approaching banks or financial institutions for home loans, it's vital to understand the eligibility criteria tailored for this category:

-

Age Limit: For self-employed individuals, the general age bracket for home loan eligibility tends to be between 21 and 65 years. This extended range often accounts for the varied retirement age among entrepreneurs and professionals.

-

Business Continuity: Lenders seek assurance of steady income, even from business owners. Typically, a business continuity of at least 3-5 years is deemed favorable as it demonstrates stability and assures lenders of consistent loan repayment.

-

Minimum Annual Profit or Turnover: The profitability or turnover of the business plays a pivotal role in dictating the loan amount that can be borrowed:

-

Annual profit of 2,00,000-5,00,000 INR: At this profit bracket, lenders might offer moderate loan amounts, ensuring the EMI aligns comfortably with the business's profits.

-

Annual profit of 7,00,000-10,00,000 INR: This profit range can lead to eligibility for higher loan amounts, especially if the business showcases consistent year-on-year growth.

-

Annual profit of 15,00,000+ INR: Businesses with such healthy profit margins are often eligible for substantial loans. Coupled with good credit history and business stability, they can also potentially negotiate for better loan terms.

-

-

Credit Report Requirement: Credit scores of 750 or above is seen as desirable. However, lenders also assess credit behavior, including past business loans and credit lines, when evaluating self-employed applicants.

-

Nature and Type of Business: The industry and domain in which the business operates can influence loan eligibility. For instance, businesses in booming sectors or those with a consistent demand (like Healthcare, E-commerce, IT & Software Services, etc.) might be viewed more favorably than volatile or high-risk industries (like Entertainment, Hospitality & Tourism, etc.)

-

Business Financials and Balance Sheet: Lenders often scrutinize the financial health of the business, including balance sheets, profit & loss statements, and cash flows for the past 2-3 years. A healthy financial record, with consistent profits and positive cash flows, can enhance home loan eligibility.

The entrepreneurial journey, while rewarding, has its financial complexities. Recognizing and aligning with the eligibility criteria of applying for home loans can simplify the process, allowing self-employed persons to inch closer to their homeownership dreams.

Also Read: Should You Buy a Freehold or Leasehold Property?

Tips to Enhance Home Loan Eligibility

While the aspirations of owning a home may be high, the eligibility for the required home loan might not match up. The good news is that with certain measures, potential borrowers can easily increase home loan eligibility, as mentioned below:

-

Clear Outstanding Loans: Reduce your existing financial obligations (Debt-to-Income ratio) as it signals to the lender that you are financially disciplined and less risky, making you a more favorable candidate for higher loan amounts.

-

Opt for Longer Loan Tenure: Longer tenure means lower monthly EMIs and banks might be more willing to approve a loan if the EMIs align comfortably with your income. However, remember that this could mean more interest paid over the tenure of the home loan.

-

Maintain a Healthy Credit Score: Your credit score acts as a reflection of your financial habits. Check your credit reports regularly, notify any discrepancies, pay your bills on time, and avoid excessive and unsecured borrowing. Follow regular positive financial activities to help boost your score over time.

-

Include a Co-applicant with Strong Credit Scores: Adding a co-borrower to the loan, especially one with a strong and stable income, can significantly improve your home loan eligibility. A joint home loan with combined income and combined responsibility will result in higher total income and reduced the bank's risk significantly. However, co-applicants with a poor credit score can adversely affect your combined eligibility, so make sure to keep an eye on their financial health.

-

Avoid Job- or Business-Hopping Just Before Applying: Frequently changing jobs or making significant business alterations shortly before applying for a home loan can raise red flags. Lenders prefer stability in employment or business as it indicates a steady source of income for the foreseeable future during the loan tenure.

-

Declare All Income Sources: Apart from your regular salary or business income, if you have other sources of income like rent, freelance work, dividends from investments, etc., make sure to declare them. This additional income can enhance your overall financial profile and potentially increase the loan amount you're eligible for.

-

Avoid Multiple Loan Enquiries: Every time you apply for a loan, the lender will pull out your credit report, leading to a 'hard enquiry'. Multiple enquiries like this in a short span can reduce your overall credit score. It's advisable to research and shortlist lenders based on your home loan eligibility before applying.

-

Reduce Credit Card Utilization: Maxing out your credit card regularly or not using it at all can negatively impact your credit score. Ideally, your credit card utilization should be below 30% of your credit limit.

-

Maintain a Strong Banking Relationship: If you've been a long-standing customer with a particular bank and have maintained a good banking relationship, it could work in your favor. Banks often provide attractive interest rates and terms to loyal customers.

-

Consider Step-Up Loans: Some banks offer 'step-up' loans where EMIs are lower in the initial years and increase gradually. If you're at the start of your career or anticipate higher earnings in the future, this might be a suitable option to enhance your eligibility now.

-

Consider Additional Collateral: Sometimes, offering additional collateral, like another property or fixed deposits, can boost your home loan eligibility. Banks often view such applications as lower risk.

Although the criteria set by banks are stringent, with a few calculated decisions, managing your finances, and optimizing your financial profile, you can greatly enhance your home loan eligibility.

Frequently Asked Questions on Home Loan Eligibility

What is the minimum salary required for a home loan?

The minimum salary varies across lenders, but typically, banks look for a salary where the EMI does not exceed 40-50% of the monthly income.

Is 720 a good CIBIL score to apply for a home loan?

Yes, 720 is a decent CIBIL score. While 750 and above is ideal, a score of 720 still indicates responsible credit behavior, increasing the likelihood of a home loan approval.

Can I get a home loan with a 695 credit score?

While 695 is slightly below the commonly preferred score of 750, many lenders still consider it. However, the loan terms might not be as favorable, and you might face a higher interest rate.

How much loan amount can I get if my salary is ₹20,000?

Assuming an interest rate of 7% p.a. for a tenure of 20 years, and considering the EMI rule (40-50% of the salary), you might be eligible for a loan amount of approx. ₹10.32 lakhs - 12.9 lakhs, with EMIs ranging from 8,000-10,000 INR.

Can I get a home loan if my salary is ₹15,000?

While it's challenging, it's not impossible. The loan amount might be lower, and terms less favorable. Opting for a longer tenure or adding a co-applicant can help.

How much loan can I get if my monthly salary is ₹35,000?

Assuming an interest rate of 7% p.a. for a tenure of 20 years, and considering the EMI rule (40-50% of the salary), you might be eligible for a loan amount of approx. ₹18.06 lakhs - 22.58 lakhs, with EMIs ranging from 14,000-17,500 INR.

Can I get a home loan if my salary is ₹40,000?

Yes. Assuming an interest rate of 7% p.a. for a tenure of 20 years, and considering the EMI rule (40-50% of the salary), you might be eligible for a loan amount of approx. ₹20.65 lakhs - 25.81 lakhs, with EMIs ranging from 16,000-20,000 INR.

How much loan can I get if my salary is ₹50,000?

Assuming an interest rate of 7% p.a. for a tenure of 20 years, and considering the EMI rule (40-50% of the salary), you might be eligible for a loan amount of approx. ₹25.81 lakhs - 32.26 lakhs, with EMIs ranging from 20,000-25,000 INR.

How much housing loan can I get if my salary is ₹80,000?

Assuming an interest rate of 7% p.a. for a tenure of 20 years, and considering the EMI rule (40-50% of the salary), you might be eligible for a loan amount of approx. ₹41.29 lakhs - 51.61 lakhs, with EMIs ranging from 32,000-40,000 INR.

How much home loan can I get on a 12 lakh p.a. salary?

For an annual salary of 12 lakhs (monthly salary = ₹1 lakh/month), you might be eligible for a home loan of ₹51.61 lakhs - 64.51 lakhs, with EMIs between 40,000-50,000 INR monthly.

How does the credit score impact loan eligibility?

The credit score is a numerical representation of an individual's creditworthiness based on their credit history. A high score indicates responsible credit behavior, making it easier to get loan approvals and favorable terms. A low score might reduce your loan amount or increase the interest rate.

What is the formula to check the home loan eligibility?

Home loan eligibility is often calculated as: Eligible Loan Amount = (Your Salary) x (multiplier, often between 50-60%) - (Any existing EMIs). Banks might have their multipliers based on internal criteria.

How to get 90% of a home loan?

A 90% loan-to-value ratio (LTV) is achievable based on the property's value, your credit score, and other eligibility criteria. However, remember that a higher LTV might lead to higher interest rates.

Is it possible to get a 100% home loan?

Getting a 100% home loan is rare in India due to the risks involved. However, some schemes or offers might provide it under specific conditions or for certain property types.

How is Home Loan Eligibility calculated on the basis of age?

Age plays a role in determining the tenure of the home loan. Younger applicants might get longer tenures, while those nearing retirement might get shorter tenures to ensure the home loan is repaid before retirement.

What are the tax benefits of home loans?

The property owner can claim tax deductions up to ₹2 lakhs on the interest paid for the home loan. If there is a co-borrower on the loan, both parties can claim tax deductions on the home loan interest based on the ratio of their ownership.

Can I enhance my eligibility for a home loan?

Absolutely. By clearing existing debts, increasing tenure, maintaining a healthy credit score, including a co-applicant, and demonstrating stability in employment or business, you can improve your eligibility.

How will my home loan eligibility change if I have multiple sources of income?

Declaring multiple sources of income can significantly improve your home loan eligibility as it showcases increased repayment capability.

Can non-resident Indians (NRIs) apply for home loans in India?

Yes, many banks and financial institutions in India offer home loans to NRIs. However, the terms, interest rates, and documentation might vary compared to resident applicants.

How do property location and type affect my home loan eligibility?

Lenders often consider the location and type of property as risk factors. Properties in prime locations or reputable projects may attract better home loan terms. Conversely, properties in areas with lower demand or in disputed regions might reduce eligibility.

How important is the employer's reputation for salaried persons?

An employer's reputation can influence the perceived stability of your income. Being employed by a reputed company might boost your loan eligibility.

Owning a home represents security, achievement, and a dream realized for many. However, the journey towards this dream often begins with understanding home loan eligibility.

Eligibility for applying for a housing loan isn't just about how much you earn or your age; it's a combination of multiple factors that lenders assess to gauge your creditworthiness and repayment capability.

Use a housing loan eligibility calculator to get a clear picture of what you can afford, plan your budget, and prevent potential financial missteps. While the initial home loan eligibility criteria may seem stringent, remember, there are always steps you can undertake to improve your housing loan eligibility. From maintaining a good credit history to considering the inclusion of a co-applicant, enhancing your eligibility is easy.

However, make sure to consult with financial advisors or bank representatives who can offer personalized advice tailored to your specific circumstances. Their insights can help you navigate the intricacies of the housing loan process more efficiently.

Lastly, always keep the necessary documentation at the ready. It's more than just ticking boxes; it's about ensuring a seamless, swift, and hassle-free home loan application process. Armed with knowledge, preparation, and a dash of diligence, your dream home might be closer than you think. Best of luck on your home-owning journey!